The New Capital Stack #41: When the Regulator Draws the Line

The line moved from discussion to decision.

[22 to 28 June 2026]

The Bank of England published the actual draft rules (reserve ratios, redemption timelines, issuance ceilings) that systemic sterling stablecoin issuers will have to operate under. Japan’s JFSA approved RLUSD as the first foreign stablecoin under its updated payment framework. Saudi Arabia’s Cabinet signed off on the geographic zones for non-Saudi real estate ownership. The US Congress passed a CBDC ban through 2030 alongside the most significant housing legislation in a generation. The BIS laid out what it thinks the monetary system should look like once tokenization scales.

Each of these is a line being drawn. Not a framework under discussion, not a working group convened, but a decision made. An asset either fits inside the perimeter or it does not. An issuer either has the license or it doesn’t. A building is either in the approved zone or outside it.

The practical question that follows is the same in every case: who has built something worth placing inside that perimeter?

TL;DR

Securitize set July 2 as its NYSE trading debut under ticker SECZ, raising ~$400M through a SPAC merger with Cantor Equity Partners II. It manages $4B+ in tokenized assets for BlackRock, Apollo, KKR, Hamilton Lane, VanEck, and BNY. (PR Newswire)

Baillie Gifford launched BAGEY on June 22, the UK’s first natively issued, FCA-approved tokenized fund: a dollar-denominated OEIC of short-duration corporate bonds targeting ~7% yield, built with BNY on Ethereum and Solana, with blockchain as the legal register of record. (CoinDesk)

Bank of England published its draft Code of Practice for systemic sterling stablecoins on June 22: per-user holding caps dropped, replaced by a £40B issuance ceiling, 70% gilt reserve backing allowed. Final rules target end-2026, with regulated stablecoins operating from 2027. (Bank of England)

Prologis disclosed a £12.6B (~$16.6B) all-share bid for SEGRO, rejected by SEGRO’s board on June 23. Prologis must make a firm offer or walk away by July 22 under UK Takeover Code. (Reuters)

The US Congress passed the 21st Century ROAD to Housing Act (Senate 85-5 on June 22, House 358-32 on June 23), including a ban on a US CBDC through 2030. Trump canceled the signing ceremony on June 24 over unrelated voting legislation. (NPR)

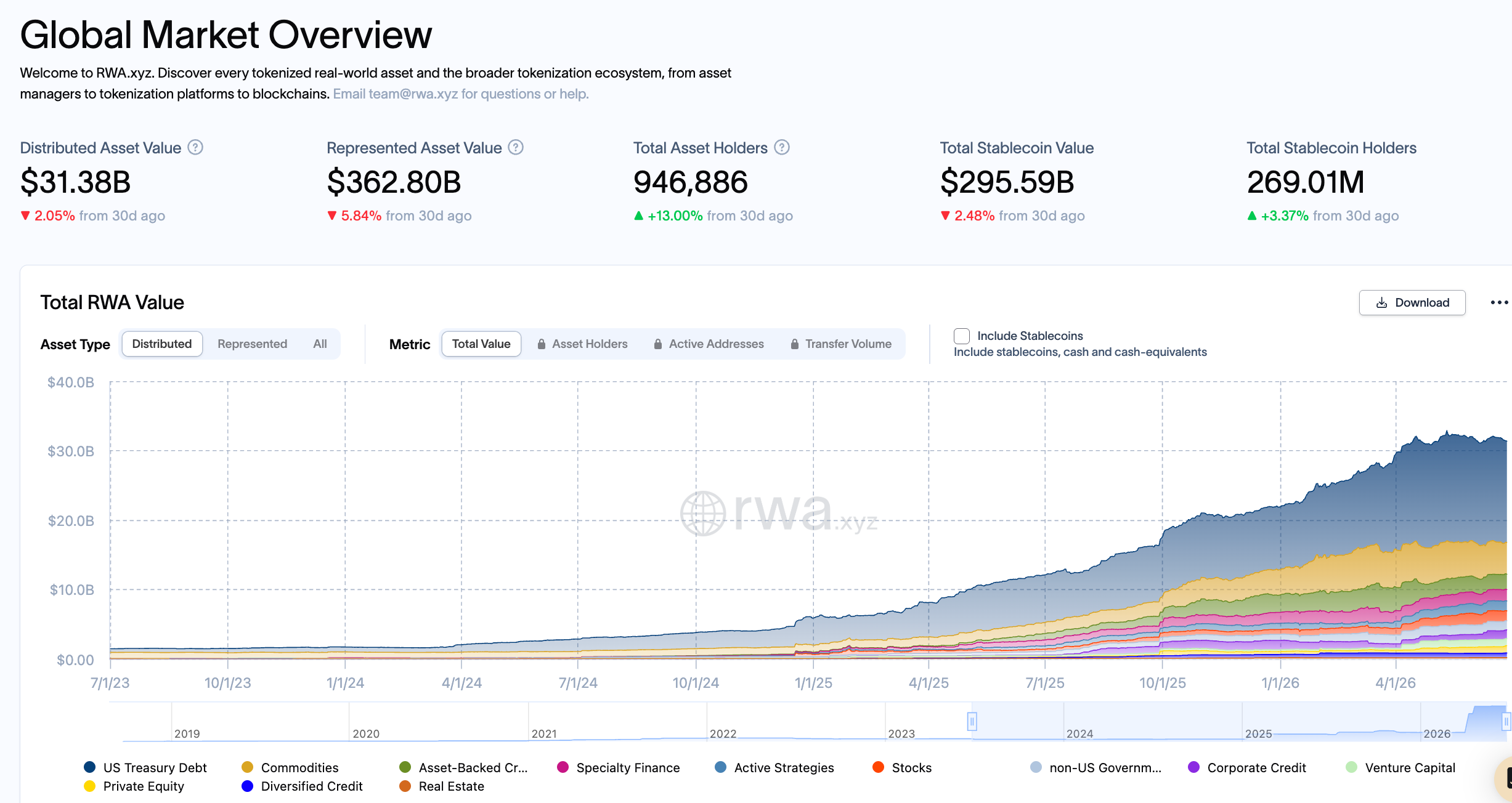

RWA market this week: Distributed asset value at $31.52B as of June 28, down from $32.28B last week and down 1.42% over 30 days. Total holders at 943,547, up from 930,159 the prior week and up 13.81% over 30 days. The pattern holds: participation keeps widening while capital contracts slightly. (Source: rwa.xyz)

RWA & Tokenization

1. Securitize goes public

Shareholder vote on June 29, merger close on July 1, NYSE trading under SECZ on July 2. The deal raises approximately $400M through the Cantor Equity Partners II SPAC, with a PIPE oversubscribed at $225M and less than 30% of shareholders electing to redeem.

Securitize manages more than $4B in tokenized assets and is the infrastructure behind funds from BlackRock, Apollo, KKR, Hamilton Lane, VanEck, and BNY. It holds an SEC-registered alternative trading system in the US and DLT Pilot Regime authorization in the EU.

A listed Securitize gives investors direct exposure to the infrastructure layer of tokenization itself: the transfer agents, compliance systems, and trading rails the market runs on. It is a bet on who owns the plumbing, and it is the bet reaching the public market first. (PR Newswire)

2. Baillie Gifford makes the blockchain the legal record

On June 22, Baillie Gifford, founded in 1908 and managing approximately £286B, launched BAGEY on Ethereum and Solana. FCA-approved UK OEIC structure, built with BNY. Target yield approximately 7% from short-duration public corporate bonds. Settled in USDC.

Most tokenized funds wrap an existing fund in a token while legal ownership stays in a traditional registry. BAGEY is different: the blockchain is the register of record, giving investors direct ownership and direct recourse. As Theo Golden, Baillie Gifford’s head of digital assets, put it: “It is a fund issued onchain, with the blockchain serving as the register of record.”

That is the detail that matters when an institutional investor’s legal counsel reviews it. The FCA’s approval under Policy Statement PS26/7 makes this replicable across the UK market. (CoinDesk, Markets Media)

3. The Bank of England publishes its actual rules

On June 22, the Bank of England published a draft Code of Practice for systemic sterling stablecoin issuers: the rules they will have to operate under from 2027, not a consultation on principles.

The headline change from November 2025: the proposed £20,000 per-user holding cap is gone, replaced by a £40B aggregate issuance ceiling per coin. Issuers may hold up to 70% of reserves in short-term UK government bonds (up from 60%), with the remainder in central bank deposits. Redemption at face value within 24 hours. No yield payments to holders.

The EU’s MiCA stablecoin rules took effect in June 2024. The US GENIUS Act was signed in July 2025. The UK’s 2027 target puts it roughly three years behind the EU, and the decision to drop holding limits reads partly as a competitiveness move. (Bank of England)

4. The Fed and the BIS draw different lines

On June 22, Fed Governor Christopher Waller framed stablecoins as new dollar channels at the Federal Reserve’s Fifth Conference on the International Roles of the US Dollar, saying they “have the potential to maintain and extend” the dollar’s global role. These were research remarks, not policy announcements. But placing stablecoins inside the dollar policy agenda rather than the crypto-supervision agenda changes the category. (Yahoo Finance)

The BIS landed differently. Its 2026 Annual Economic Report argued that stablecoins fall short of the core features of money and that private stablecoin adoption creates risks for bank funding and monetary sovereignty. Its position: tokenized finance should stay anchored to the two-tier monetary system, not develop as a parallel private money layer. (BIS)

The gap between them is not a disagreement about technology. It is a disagreement about who controls the settlement layer.

5. ICE and OKX build the distribution layer

On June 22, Intercontinental Exchange (the NYSE’s parent) and OKX announced a 50/50 joint venture, subject to regulatory approval, targeting operation as a US-registered broker-dealer and futures commission merchant. OKX’s 120+ million users would access ICE futures and NYSE tokenized equities. NYSE infrastructure gets crypto-native distribution.

The bet is on architecture, not product. Whether the regulatory approval materializes is the open variable. (Business Wire)

6. Japan approves the first foreign stablecoin

On June 24, Ripple and SBI Group launched RLUSD in Japan following JFSA approval, classified as a Type 4 electronic payment instrument under Japan’s Payment Services Act. It is the first foreign-issued stablecoin cleared under Japan’s updated framework. Available through SBI VC Trade to institutional and retail users. $1.7B market cap, backed 1:1 by US dollar deposits and short-term Treasuries.

One caveat worth noting: RLUSD transactions in Japan are capped at one million yen (~$6,200). That is a retail ceiling, which sits awkwardly against Ripple’s institutional positioning and limits the use cases until the cap is revised. (Ripple, The Asian Banker)

7. Transfer agents enter the tokenization stack

Continental Stock Transfer and Trust, part of the traditional issuer-record and shareholder-administration system underpinning US public markets, selected Securitize as a preferred tokenization partner covering SPACs, IPOs, and publicly traded companies.

Tokenization at an institutional scale requires more than issuance technology. It requires transfer agents, investor records, and shareholder servicing: the machinery that makes ownership legally functional. When Continental selects a tokenization partner, that choice propagates across every issuer in its network. (PR Newswire)

8. The market is wider, not yet deeper

Franklin Templeton completed its acquisition of 250 Digital on June 22, establishing Franklin Crypto as a permanent active digital-asset management division with $1.78T in group AUM behind it. Not a pilot. (Franklin Templeton)

Also notable: two tokenized tranches of the Mubadala Capital Alternative Solutions Fund registered on rwa.xyz on June 26 via KAIO, totaling approximately $64.7M. Mubadala manages over $430B in assets. The partnership was announced in January; this week’s registration marks the funds going live rather than an intent to explore. Sovereign-linked private equity onchain is early, but it is the harder tokenization problem: illiquid, long-dated, complex to administer. Getting it right expands the addressable RWA market well beyond fixed income.

The rwa.xyz data frames both: distributed value at $31.52B, down from $32.28B the prior week, while holders grew to 943,547. More participants, less total capital. The infrastructure being built is designed to close that gap.

Real Estate Pulse

1. The SEGRO bid and what logistics is actually worth

Prologis disclosed a £12.6B (~$16.6B) all-share bid for SEGRO, the UK’s largest listed industrial and logistics landlord. SEGRO’s board rejected it unequivocally on June 23. Prologis went public with the terms on June 24 and urged shareholders to press the board to engage. Under the UK Takeover Code, Prologis must make a firm offer or walk away by July 22.

The premium was 24.6% of the prior close, equal to SEGRO’s NAV per share as of December 2025. Prologis argued integration would unlock value from SEGRO’s logistics, power, and data center development pipeline. The UK REIT sector moved on the disclosure: Land Securities up approximately 4%, with British Land, LondonMetric, and Tritax Big Box also rising.

Even if the bid lapses, it forces a reappraisal of European logistics at a moment when warehouses with power access and data-center optionality are competing directly with traditional real estate for institutional capital. The BlackRock-backed AIP interest in STACK Data Centers sits in the same frame. (Reuters, Bloomberg)

2. US housing supply: the bill passed; the problem didn’t

The 21st Century ROAD to Housing Act cleared the Senate 85-5 on June 22 and the House 358-32 on June 23, the most significant US housing legislation since 1990. It targets supply: zoning reform, streamlined permitting, limits on institutional single-family home buying, and a ban on a US CBDC through 2030. Trump canceled the signing ceremony on June 24, tying the bill to separate voter-ID legislation. Speaker Johnson indicated he would likely sign before the 10-day automatic enactment window closes.

The political signal is real. The market reality is separate. Bipartisan supply-side reform does not change mortgage rates, construction costs, or developer margins. Savills published data the same week showing England will deliver roughly 837,500 new homes over five years to 2029/30, against a government target of 1.5 million. Legislative clarity is a necessary condition. It is not a sufficient one. (NPR, Savills)

3. US commercial real estate: prices fell across both segments

CoStar’s May CCRSI showed both the value-weighted and equal-weighted composite indices declining simultaneously for the first time in 2026: value-weighted down 0.6%, equal-weighted down 1.3%. The office posted the steepest declines. Transaction counts are down approximately 20% year-over-year. The value-weighted index sits 16.4% below its July 2022 peak.

Capital is sorting by income quality and sector, not retreating from commercial real estate broadly. That is the environment any tokenized commercial real estate product enters. A token does not change the underlying asset’s cash flows, financing costs, or appraisal direction. (CoStar)

4. Saudi Arabia opens the zones

Saudi Arabia’s Cabinet approved the executive regulations for non-Saudi real estate ownership on June 23, including the specific geographic zones. The base law took effect in January 2026. This week’s approval is the operational layer that makes it usable.

Approved zones include parts of Riyadh, Jeddah, Makkah, Madinah, AlUla, and giga-projects including NEOM, Amaala, and the Red Sea project. All transactions route through the “Saudi Properties” digital portal. The market is valued at approximately $77B, with IMARC Group projecting growth toward $141.6B by 2034. The foreign ownership framework is one lever behind that projection, not the only one. (Arab News, Gulf News)

5. Dubai: volume holds at the quality end

Economy Middle East reported approximately $75B in new project launches across Dubai in 2026. fäm Properties facilitated the sale of 40,000 sq ft of Grade A office space at Vision Tower in Business Bay for AED 124M (~$34M) on June 24, described as the largest commercial office deal of its kind recorded in Dubai.

Developers are still launching at scale and institutional-grade assets are still transacting. The open question is whether a $75B pipeline absorbs cleanly if geopolitical risk or affordability pressure persists. At the right quality threshold, buyers remain present. (Economy Middle East, Zawya)

OneAsset POV: The Line Is Written Before the Product

The week’s pattern was consistent across every jurisdiction. The Bank of England drew a line: here is what a compliant sterling stablecoin looks like, here is what it cannot do, here is who gets to issue one.

Japan drew a line: here is the first foreign stablecoin that cleared our framework.

Saudi Arabia drew a line: here are the zones, here are the conditions, here is the portal.

The US drew a line: no CBDC, which means private infrastructure fills the space.

Every one of those lines was drawn before any product operated inside it. That sequencing is not incidental. It is the point.

The argument for building compliance-first infrastructure, before the product is live, before the market is deep, before the regulator has finished writing the rules, is that when the line gets drawn, you are already on the right side of it. Baillie Gifford did not launch BAGEY and then seek FCA approval. The FCA approval is what made BAGEY possible. Ripple did not expand into Japan and then engage the JFSA. The JFSA decision is what the Japan expansion is. Securitize did not build a tokenization platform and then worry about SEC registration. The SEC registration is the platform.

The missing layer in tokenization is not issuance technology. It is enforceable rights: the legal architecture that makes a token mean something when an institution tests what it actually owns. That architecture is written before the product launches, in the structure of the instrument, in the regulatory standing of the issuer, in who holds the asset and who can enforce against it.

For commercial real estate specifically, the environment makes this harder to ignore. US commercial prices fell across both segments in May for the first time this year. Saudi Arabia just opened its zones, which means early positioning matters, but so does the compliance framework you bring to a new jurisdiction. Dubai is transacting at the quality end while the broader pipeline carries absorption risk.

None of that changes with a token. What changes is whether the token carries a real claim, one that holds up under the conditions the market is actually in, not the conditions of a press release. The infrastructure that got licensed, listed, and codified this week is the foundation that makes a real claim possible. The rest is the work of being inside the perimeter before the line moves again.

Disclaimer: This summary is based on published sources and does not constitute investment advice. While we strive for accuracy and timeliness, projects like this may have changed since the last available reports.

About OneAsset

OneAsset is a Dubai-based real-world asset tokenization company building compliance-first infrastructure for institutional commercial real estate. Purpose-built for the full lifecycle of tokenized real estate, OneAsset supports the systems required for compliant issuance, servicing, reporting, ownership controls, transfer rules, and lifecycle management. The company brings the structural discipline of commercial real estate into onchain market infrastructure, with regulated deployment readiness from the start.

Join the waitlist for launch access, or follow along for what we’re seeing across the market.

X | Website | LinkedIn | Instagram

Subscribe to The New Capital Stack for the weekly read.